I have been trying to get in roots with the “SCIENCE” part of

Actuarial Science. Actuarial Exams are absolutely loaded with material on “probability”

and entailing Loss Models but the world has now moved on to bigger things like

Big Data and GLMs, Extreme Value Theory and Solvency II (it’s probably all they

can tweet about).

It’s all the more important to get the amassed knowledge accounted

for and get our facts straight but I think it’s equally important to develop

our tool kit and use technology at our aid. This is the part that excites me

the most and while for the past few months I have been trying to get hands on

practice at probability models, model fitting, and some quantitative finance

related mathematics, everything while using MAPLE 18 at my aid.

However, usually in my ambition I don’t get much done but rather lose

track and go off on a tangent.

The Beginning

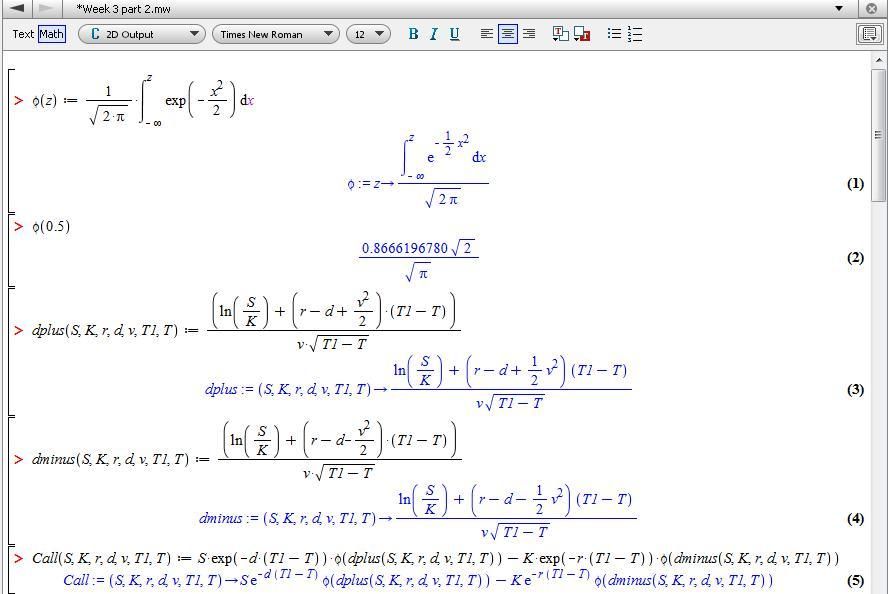

Primarily,

MAPLE appeals to the ease of writing mathematical functions and notations; it

skips the long codes and lets mathematicians do what they are good at. Writing

a call option function was as easy as:

Hence, a call value was easily computable by substituting values

for respective parameters in the function. Further, Greeks for the call were

easily computable by writing differentials with respect to the parameter of

choice.

And so it progressed….

What followed was me getting carried away, trying to do everything

on MAPLE. The madness was in check while I studied “Linear Algebra” with the

aid of MAPLE, however it did start to get unhealthy after a while when I

decided to solve the Loss Models book on it.

As a life actuary although exposed to a wide array of Loss Models

in exams, I never get to apply them although some of them I believe would soon

be coming in handy for say modeling claim reporting lags, short term group

contracts and definitely catastrophe modeling.

Fiddling with the CIR

Interest Rate models are my biggest bother and I haven’t yet quiet

wrapped my head around how any model let alone single factor models can emulate

interest rate movements. It’s because interest rates don’t have a code or a

system; they don’t even exhibit the Brownian motion characteristics of stock

prices. I have seen Least Square calibrations of Cox-Ingersoll many times but have

never quite agreed with the results.

Of course users would argue that such models are essentially for

short durations and hence any systematic change in the economy can damage the

results.

Through Wiki, I learned that the Cox-Ingersoll essentially has a “Non-central

Chi-squared distribution” for future rates and had this ambitious idea to

calibrate the model using Maximum Likelihood. What followed was me trying to

calibrate daily US treasury rates for a period of a year and a half having

approximately 350 instances.

Suffice to say that the calibration failed and I realized I was basically

asking MAPLE to do too much iteration. So that was more than 2 hours of my life

I won’t get back but I live to fight another day.

And then the Loss Models madness

I must have been in desperate need for some intellectual

stimulation if I decided to solve the Klugman book (which I was rather scared

of during the Exam C days).

It was good discovering the wide array of built-in probability distributions

and the ease with which PDFs, CDF, MGFs, etc can be used. Also impressive are

the built in Maximum Likelihood methods and Hypothesis testing.

What

followed was me exploring distributions I have never quiet worked with before.

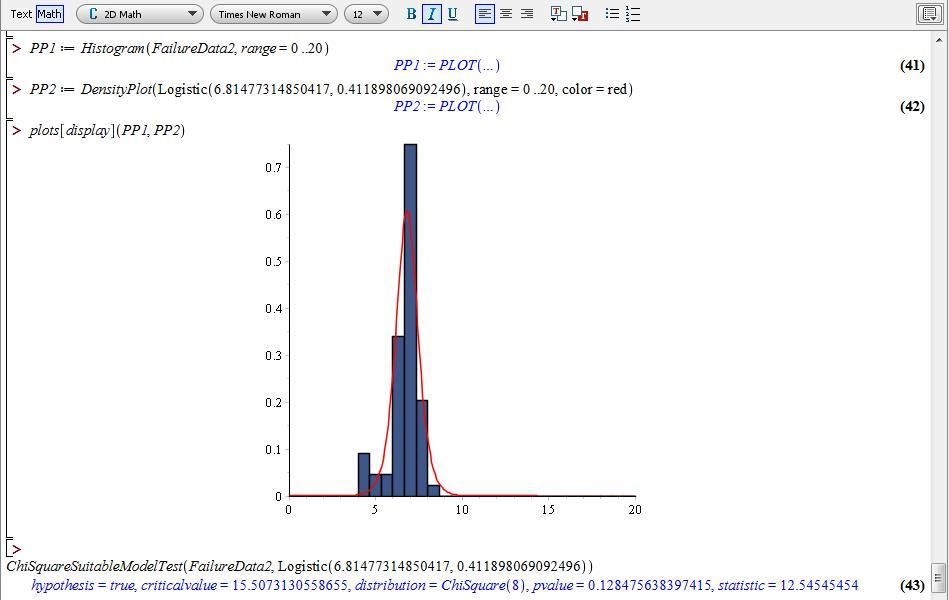

A log-logistic distribution calibration on time to failure data of some

submarine part was one of the successful calibrations and so detailed a utility

for the model:

However, I ended up spending too much time learning to

and then solving rather easy problems just for the pleasure of solving them by software.

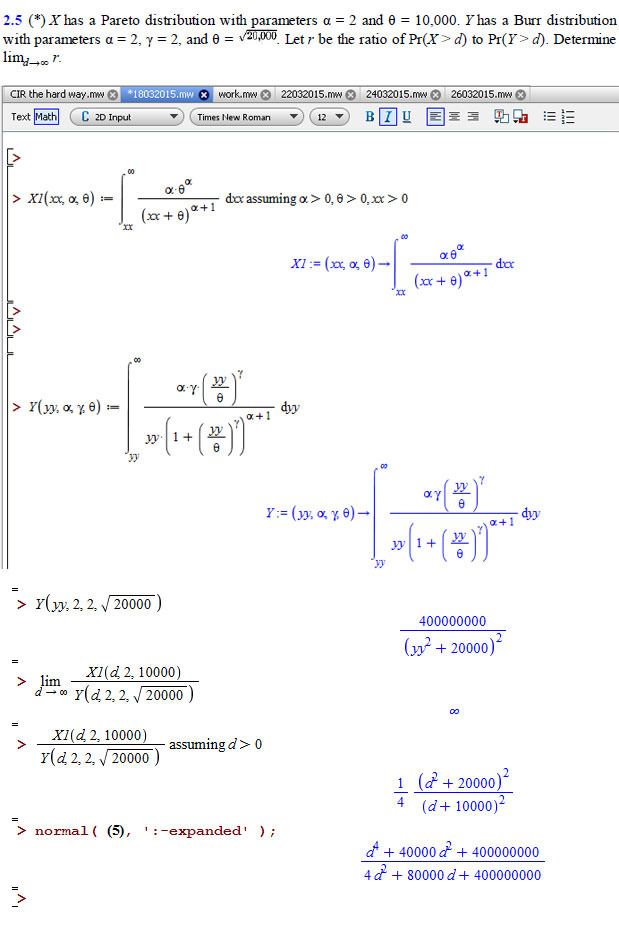

The following must have taken at least 10 minutes at first to learn to write

and solve:

However, once I had the hang of it I was doing problems and

plotting curves for the fun of it.

When I finally stopped

It was all an attempt again to seek mastery over the subject

matter while learning new software but the more you work with probability

models the harder it becomes to acknowledge them as interesting and worthwhile.

This follows a feeling of frustration of yet again failing to acquire even a

little sense of accomplishment and an inside echo reminding you of what your

life has become.

This guy tells it best:

when your computer dies and you're forced to see the mess you've become pic.twitter.com/QtpFdYuUGc

— Tyler Oakley (@tyleroakley) October 25, 2014

amazing journey. very few have the courage to be so honest and blunt

ReplyDeleteCommendable writing skills man, just the right amount of wit. I wish I could be learned enough when it comes to complex distributions.

Delete